Article Summary

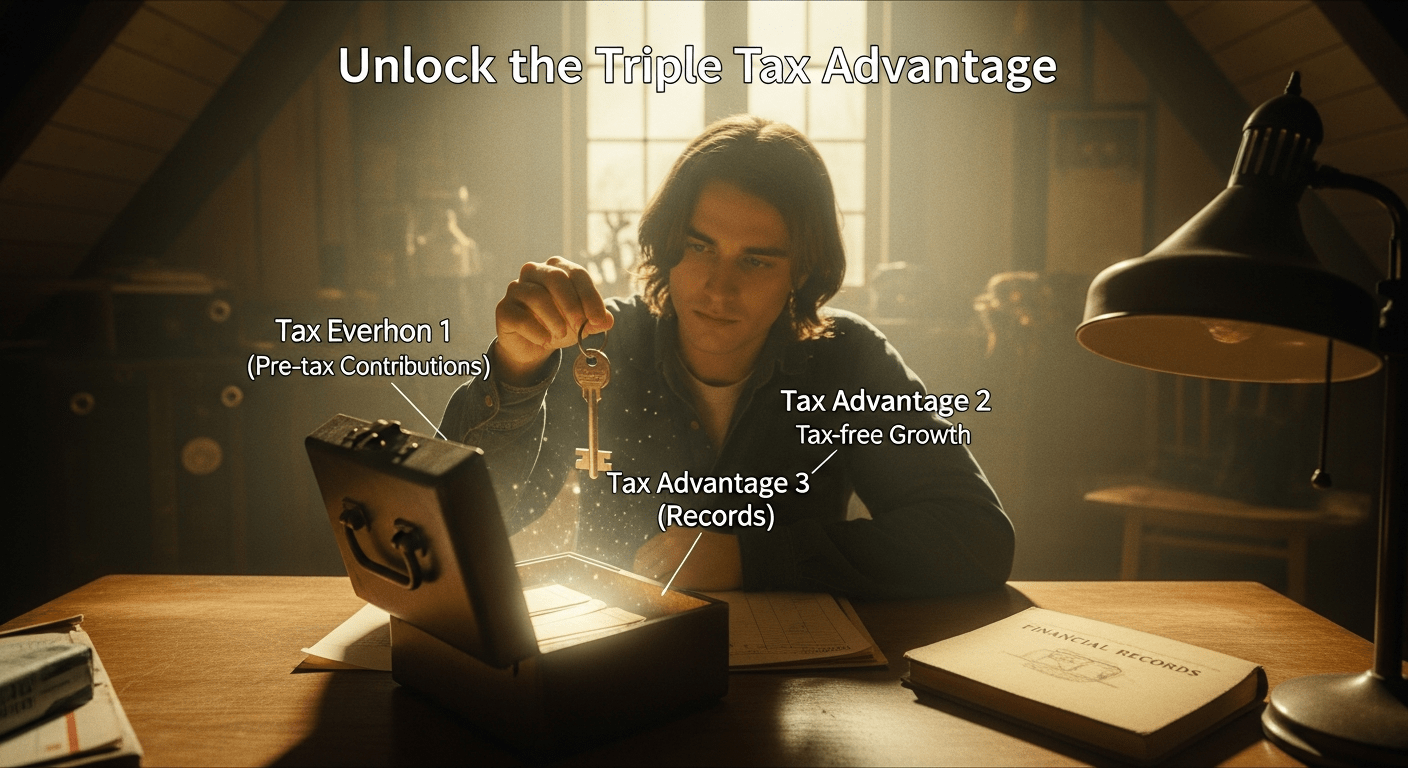

- The HSA triple tax advantage offers pre-tax contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses, making it an elite retirement tool.

- Learn how to maximize HSAs alongside 401(k)s and IRAs for compounded retirement savings with real-world calculations.

- Discover eligibility rules, investment strategies, and action steps to implement the HSA triple tax advantage today.

Health Savings Accounts (HSAs) deliver the HSA triple tax advantage, a rare financial benefit that positions them as one of the most powerful tools for retirement savings. This unique structure allows contributions to grow tax-deferred, earnings to accumulate tax-free, and qualified withdrawals to escape taxes entirely—provided they’re used for medical expenses. For everyday consumers planning for retirement, understanding and leveraging the HSA triple tax advantage can significantly boost long-term wealth, often outperforming traditional savings vehicles.

What is the HSA Triple Tax Advantage?

The HSA triple tax advantage refers to three distinct tax benefits that make HSAs stand out in personal finance. First, contributions are made with pre-tax dollars, reducing your taxable income in the year you contribute. Second, all investment growth within the account—interest, dividends, and capital gains—accumulates entirely tax-free. Third, withdrawals for qualified medical expenses are tax-free, even in retirement. This trifecta is unmatched by most other accounts, as noted by the IRS, which outlines these rules clearly for eligible individuals.

Consider a typical family: If you contribute the maximum allowable amount annually, say around $8,000 for family coverage based on current guidelines, that immediately lowers your federal tax bill. For someone in the 22% tax bracket, this saves about $1,760 in taxes upfront. The funds then invest and grow without the drag of annual taxes on gains, compounding more efficiently. In retirement, when medical costs often surge—data from the Bureau of Labor Statistics indicates healthcare expenses rise sharply after age 65—you can withdraw tax-free, preserving more of your nest egg.

How the Three Tax Benefits Work in Practice

Pre-tax contributions lower your adjusted gross income (AGI), potentially qualifying you for other tax breaks like credits or deductions. Tax-free growth means no capital gains taxes on stock sales inside the HSA, unlike taxable brokerage accounts. Tax-free qualified withdrawals cover everything from doctor visits to prescriptions, and after age 65, even non-medical withdrawals are penalty-free (though taxed as income).

Financial experts recommend prioritizing HSAs over Roth IRAs for high-deductible health plan (HDHP) holders because of this edge. According to research from the National Bureau of Economic Research, tax-advantaged accounts like HSAs lead to higher lifetime savings rates among participants.

To illustrate, suppose you contribute $4,000 annually to an HSA. At a conservative 5% annual return, after 30 years of compounding tax-free, it grows to over $230,000. In a taxable account, the same contributions might net only $150,000 after taxes on gains. This disparity underscores why the HSA triple tax advantage is a cornerstone of retirement planning.

This section alone highlights why everyday savers should view HSAs not just as healthcare funds but as supercharged retirement vehicles. The IRS states that unused funds roll over indefinitely, allowing accumulation for decades.

Why HSAs Excel as Retirement Savings Tools

Beyond the core HSA triple tax advantage, HSAs function like IRAs for retirement because balances carry over year to year with no “use it or lose it” rule. This permanence enables long-term investing, turning healthcare savings into a retirement powerhouse. The Consumer Financial Protection Bureau (CFPB) emphasizes HSAs’ flexibility for future medical needs, which often comprise a large portion of retirement spending.

In retirement scenarios, healthcare can consume 15-20% of budgets, per Federal Reserve data on household expenditures. An HSA covers these costs tax-free, freeing up other retirement accounts. Moreover, post-65 non-medical withdrawals incur only income tax—no 10% penalty like early IRA withdrawals—making it versatile.

Real-World Retirement Impact of the Triple Tax Edge

Strategies include aggressive investing early (stocks for growth) and conservative shifts later (bonds for preservation). This mirrors 401(k) allocation principles but with superior tax treatment.

- ✓ Confirm HDHP eligibility annually

- ✓ Invest HSA funds beyond cash for compound growth

- ✓ Track receipts for reimbursement to preserve tax-free status

Compared to emergency funds, HSAs offer liquidity with tax perks. The triple tax advantage amplifies every dollar, making it essential for holistic retirement planning.

Found this guide helpful? Bookmark this page for future reference and share it with anyone who could benefit from this financial advice!

Eligibility Rules and Contribution Strategies

Unlocking the full HSA triple tax advantage starts with eligibility: You must be enrolled in a high-deductible health plan (HDHP) with minimum deductibles set by the IRS, typically around $1,500 for individuals or $3,000 for families. No other coverage like Medicare disqualifies you, but being uninsured doesn’t qualify either.

Contribution limits adjust periodically but hover around $4,000-$8,000 annually, plus $1,000 catch-up for those 55+. Employer contributions count toward limits but are tax-free to you. The IRS provides detailed tables for these, ensuring compliance preserves the tax benefits.

Maximizing Contributions for Optimal Tax Savings

Strategy one: Contribute the maximum via payroll to capture pre-tax savings and any employer match—up to 100% in some plans. Strategy two: Front-load early in the year for maximum compounding time. For self-employed, deduct contributions on Schedule 1, amplifying the triple tax advantage.

Contribution Cost Breakdown

- Annual max family contribution: ~$8,000 (pre-tax savings: $1,760 at 22% bracket)

- Catch-up (age 55+): +$1,000 (extra $220 savings)

- Employer match average: $1,500 (free money, fully vested)

Avoid over-contributing, which incurs 6% excise tax. Bureau of Labor Statistics data shows average families contribute only 20-30% of limits—leaving billions in untapped tax advantages.

Actionable: Use IRS Publication 969 for rules. This foundation ensures the HSA triple tax advantage works for you long-term.

Investment Options and Growth Strategies Inside HSAs

Many HSAs default to low-yield savings (1-2% APY), but to harness the HSA triple tax advantage, shift to investments. Providers like Fidelity or Vanguard offer brokerage windows with stocks, ETFs, and mutual funds—tax-free growth supercharges returns.

Current rates suggest balanced portfolios yield 5-8% long-term. The Federal Reserve’s historical data on asset classes supports diversified investing: 60% stocks/40% bonds for ages 40-60, gliding to conservative later.

Building a Diversified HSA Portfolio

Start with low-fee index funds (expense ratios under 0.1%). Example allocation: S&P 500 ETF (50%), international stocks (20%), bonds (30%). Rebalance annually to lock gains tax-free.

| Investment Option | Avg Annual Return | Risk Level |

|---|---|---|

| Cash/Money Market | 1-3% | Low |

| Balanced Funds | 5-7% | Medium |

| Stock ETFs | 7-10% | High |

HSA Investing Guide details provider comparisons. This approach turns HSAs into retirement multipliers.

Comparing HSAs to Traditional Retirement Accounts

The HSA triple tax advantage gives HSAs an edge over 401(k)s (pre-tax in, taxed out) and Roth IRAs (post-tax in, tax-free out). No account matches all three benefits. CFPB comparisons highlight HSAs’ healthcare specificity as a retirement differentiator.

| Pros of HSAs | Cons of HSAs |

|---|---|

|

|

Integration with 401(k) and IRA Strategies

Priority order: Max employer 401(k) match, then HSA for triple tax advantage, then IRA. This layers benefits. IRS data shows combined use yields 20-30% more after-tax retirement income.

For example, $10,000 across accounts: HSA grows most efficiently due to no RMDs (required minimum distributions). Retirement Account Comparison expands on this.

Common Pitfalls and How to Avoid Them

Many forfeit the HSA triple tax advantage by leaving funds in cash or spending early. Pitfall one: Cash drag—average HSA yields 1%, vs. 7% market. Solution: Invest post-emergency buffer (3-6 months deductible).

Pitfall two: Non-qualified withdrawals before 65 trigger taxes + 20% penalty. Track expenses for future reimbursement—IRS allows retroactive claims anytime.

Tax Compliance and Reimbursement Strategies

Pitfall three: Provider fees eroding returns—choose low-cost custodians. Federal Reserve studies show fees reduce wealth by 1% annually compounded.

- ✓ Audit HSA annually for compliance

- ✓ Switch providers if fees >0.5%

- ✓ Name beneficiaries to avoid probate

Avoiding these preserves the full power. HSA Mistakes Guide.

Actionable Steps to Implement Your HSA Retirement Plan

To capture the HSA triple tax advantage, follow this roadmap. Step one: Enroll in an HDHP if eligible—compare premiums vs. deductibles for net savings.

Step-by-Step Implementation Guide

- Confirm eligibility via IRS rules.

- Open/invest HSA with a brokerage provider.

- Automate max contributions.

- Build diversified portfolio.

- Monitor and rebalance yearly.

Integrate with overall plan: Use HSA for healthcare, 401(k)/IRA for general. BLS data underscores rising medical costs, making this vital.

Frequently Asked Questions

What exactly is the HSA triple tax advantage?

The HSA triple tax advantage consists of pre-tax contributions that reduce taxable income, tax-free growth on investments, and tax-free withdrawals for qualified medical expenses. This makes HSAs uniquely efficient for long-term savings.

Can I use my HSA for retirement beyond medical expenses?

Yes, after age 65, non-medical withdrawals from HSAs are penalty-free and taxed only as ordinary income, similar to a traditional IRA, while preserving the core tax advantages for medical use.

What are the current HSA contribution limits?

Limits are set annually by the IRS, typically around $4,000 for individuals and $8,000 for families, with an extra $1,000 catch-up for those 55+. Check IRS guidelines for precise figures.

Are HSAs a good investment for retirement?

Absolutely—the HSA triple tax advantage, combined with no required distributions and rollover flexibility, positions HSAs as superior to many retirement accounts for healthcare-heavy retirements.

How do I invest my HSA funds?

Select providers offering investment options like ETFs and mutual funds. Aim for diversified, low-fee portfolios to maximize tax-free growth, treating it like a retirement brokerage account.

What happens if I change jobs or health plans?

HSAs are portable; funds stay yours regardless. However, maintain HDHP coverage to contribute—losing it pauses new contributions but doesn’t affect existing balances or the triple tax advantage.

Key Takeaways and Next Steps

The HSA triple tax advantage transforms healthcare savings into a retirement juggernaut: pre-tax in, tax-free growth, tax-free medical out. Prioritize maxing it after employer matches, invest wisely, and save receipts. Real-world math proves $100,000s in extra wealth.

Next: Review your plan, Explore HDHPs, consult pros. Consistent action unlocks this powerhouse.